Flipping Through 30 Years of Fintech in Nigeria

How did the fintech space evolve in the last three decades, and what’s next for the industry in Nigeria?

Nigeria seemingly has the perfect environment for a thriving fintech sector; a young vibrant population, increasing smartphone penetration, and a focused regulatory drive to increase financial inclusion and cashless payments.

But it wasn’t always like this.

How did the fintech space evolve in the last three decades, and what’s next for the industry in Nigeria?

Come along and I will quickly take you through 30 years of fintech’s evolution in Africa’s most populous nation.

There are over a hundred movies with a plot centred on the assassination of the American president, but Vantage Point stands out for me.

The brilliance of the 2008 American political action thriller film is something logical yet profound: it tells an incident from the perspectives of different characters.

The President of the United States is in Salamanca, Spain, about to address the city in a public square. There’s a jubilant crowd with a few protesters, a cop in plain clothes, his girlfriend with another man, a mother and child, an American tourist with a video camera, and a Secret Service agent newly returned from medical leave.

As the President gets called onstage to give his speech, shots ring out and the President falls. A few minutes later, there’s a distant explosion and then a bomb goes off in the square.

Those minutes are retold several times, emphasising different characters' actions. As the movie plot progresses and those minutes are retold, a clearer picture of the actual events unfolds. Case in point: halfway through this movie, if you think you got it all figured out, you haven't got a clue. Ultimately, the movie highlights an important lesson of how we should question the occurrence of an event because not everyone sees things from the same perspective.

An attempt to chronicle the evolution of fintech Nigeria is audacious, so I’ll try to do that by taking into account as many perspectives as I can. To simplify things I’ve had to largely rely on the perspective of banks, startups, consumers, and regulators.

Back to the Origin

It’s difficult to place where the fintech revolution started but I’ll largely attribute it to when financial institutions moved from solely relying on paper records to using computer software. In 1991, John Obaro gave up a plush job as a banker to resell financial software, setting up SystemSpecs.

👉🏾 RECOMMENDED READ: ‘SystemSpecs: A Transgenerational (Fin)Tech Company’

It’ll take another three years before they’ll start thinking about building local software to solve Nigerian problems, and an additional five before a payment feature initially meant for a product was spun off as a standalone product – Remita. At first, the Nigerian economy was reliant on foreign software.

Over the next five years, the Central Bank of Nigeria and commercial banks will come together to form two important entities: a de facto payment system regulator and a card payment company.

First, in 1993, the Nigeria Inter-Bank Settlement System (NIBSS) was founded and owned by all licensed banks including the Central Bank of Nigeria. It’ll take another two decades before NIBSS will rise to its full potential by creating NIP (NIBSS Instant Payment), an online real-time Inter-bank payment solution and NAPS (NIBSS Automated Payment Services). These solutions facilitated interbank transactions.

Then four years after the creation of NIBSS, a consortium of Nigerian banks came together to set up the country’s first electronic payment company, Unified Payments, then known as SmartCard Nigeria Plc. Its most important contribution was when it started rolling out a card scheme for Nigerian banks by the year 2000.

Global payment giant Visa got wind of this and invested in this company; extending its reach into Nigeria. This partnership enabled it to become a principal partner of Visa in 2006, allowing Nigerian banks to issue payment cards to Naira account holders to be used for the first time globally.

Over the past 15 years, Unified Payments has expanded its services to include a switch service, agency banking, and a value-added services platform that offers customers access to services which include the purchase of Airtime.

A new millennium and new entrants

The dawn of the new millennium saw Nigeria experience increased connectivity due to the privatisation of the telecoms sectors – the total number of telephone connections rose from about 400,000 in 2000 to over 4 million in 2003.

Brilliant entrepreneurs started looking into what business opportunities this new technology could bring. One of them Mitchell Elegbe was able to marshall a ₦200m ($1.2m) equity deal from some Nigerian banks to finance his new company Interswitch. At that time it didn’t matter that he didn’t have a stake in the company.

“I don’t know if you are aware, but when I started Interswitch I did not have a single share in the business… and I gave up 100% ownership,” Elegbe said in an Interview.

But what Elegbe gave up in terms of ownership, he made up in terms of fast growth. Interswitch, which started as a payment switch for banks, expanded its offering to include payment gateways, merchant acquiring services, mobile money platforms, and e-commerce solutions. Its Verve card scheme is the most successful one by a local company with over 50 million active payment cards. At least 50% of card payments made in Nigeria are made with Verve cards. The company has also made inroads in East Africa – Kenya and Uganda.

Interswitch’s ubiquitous product lines and fast growth were reflected in the company’s valuation in 2010 when the second infusion of capital came through private equity investment. Helios Investment Partners acquired a 66.67% stake in the company. Interswitch was valued at ₦26bn ($163m), according to Elegbe. By 2019, Interswitch’s valuation had ballooned to $1 billion with Visa acquiring a 20% stake.

When you’re backed by Nigerian banks, navigating the murky waters of the financial systems is easier — not necessarily seamless though.

Founded a year after Interswitch, eTranzact followed a somewhat different route. 38-year-old Valentine Obi saw an opportunity to reduce the amount of cash in circulation. eTranzact focused solely on being a payment switch and gateway with some attempts at rolling a card scheme that didn’t pan out as expected. Still, it pioneered mobile banking, USSD, and cardless withdrawal. It provided interbank switch service before NIBSS became functional.

👉🏾 RECOMMENDED READ: ‘eTranzact: The most valuable Nigerian publicly listed fintech company’

Being the only pure-play fintech company listed on the Nigerian stock exchange revealed a few things about the intricacies of being a regulated financial service company. Its existence has been threatened more by fraud and sanctions than new entrants in the space.

Mobile Money

Mobile Money – the ability to store, send and receive money through mobile devices – offered a faster path to financial inclusion but the apex regulatory body had always been sceptical about giving powers to non-financial institutions.

Until 2009, when the CBN introduced the regulatory framework for Mobile Money Services in Nigeria. Later that year, Tayo Oviosu co-founded Paga, a mobile payments company with Jay Alabraba. The company name Paga is a Spanish word that means “to pay”. Paga will go on to popularise mobile money among the unbanked in Nigeria.

By 2011, the CBN issued its first set of mobile money licenses, companies like Paga, eTranzact, MKudi, FETS Limited were among the first non-bank-led mobile money operators to get a license.

While mobile money became regulated in the early 2010s, mobile money activities had been in existence since as early as 2005. Here’s Niyi Tolulope, eTranzact CEO recounting an experience in 2005.

There was a World Bank-assisted project where some of the [eTranzact] executives went to Kano State to pitch cattle rearers and traders. We were presenting this e-wallet that day and one Alhaji stood up and said “So you can put money in this wallet and I will travel and nobody knows there is money in it? And when I get there I can use it?” All of us said “Yes”. The man brought out ₦200,000 cash and said, “Put this in the wallet.” We signed him up immediately. He was probably one of the first people we had back then.

Commercial banks also hopped on the mobile money train. So far 13 out of 24 Commercial Banks are licensed mobile money operators.

2010s: Beyond Payments

With the foundations of payment infrastructure being laid, the next decade ushered in a wave of new fintech companies like VoguePay (2012), Paystack (2015), MoniePoint (known as TeamApt in 2015), Flutterwave (2016), and PalmPay (2018).

New use cases were found and financial/ banking services were unbundled. This was also aided by improvements in internet penetration, national identity system and supporting regulatory frameworks.

Piggy Vest (2016) and Cowrywise (2017) – Saving and Investment

Trove (2018) and RiseVest (2019) – Wealth management

Migo (2013) and Fair Money (2017) – Digital lending

Wallets Africa (2018) and Opay (2018) – Mobile wallet

Helicarrier (2017) and Quidax (2018) - Crypto

One Pipe (2018) and Mono (2020) – Embedded finance/ API

Prospa (2019) and Brass (2020) – Business Banking

A map of the Nigerian Fintech space

Here’s how some of these startups came about. Ambitious individuals saw an opportunity to leverage existing technology to solve different problems.

Piggvest, formerly known as Piggybank, started with a simple idea of automating standing orders for payments to enable effortless saving of funds. What would have required visiting the bank to fill out a form was replaced with a few clicks. And it worked seamlessly. Before the predatory lenders came online, Migo and Fair Money figured out how to lend money digitally without running out of business.

As the crypto revolution was picking up steam Hellicarrier (then known as Buycoins) and Quidax saw an opportunity in providing a marketplace/exchange for people to buy and sell cryptocurrencies. This was a better option than trading with a total stranger on Telegram or Twitter.

By democratising access to global and local stocks Trove and RiseVest unlocked a burgeoning retail investment market. They made it easier for people to have wealth management services which had been sort of exclusive to high network individuals.

Digital wallets were offered as a better alternative to traditional bank accounts which often had down times and complicated rules around how funds were moved. While it wasn’t exactly true, as the digital wallets were often also reliant on the same infrastructure (think: NIBBS) that banks relied on, the optionality of having your funds in different places made it worth trying them out. Wallets Africa and OPay made this popular.

The list of innovations goes on and on.

The proliferation of fintech startups has raised questions such as whether there are too many fintech startups. Yes, there’s a disproportionate amount of fintech companies in Nigeria but I disagree that there are too many fintech companies. The real concern is that too many fintech companies are playing in the same sub-sector: Payment. Almost half (43%) of the 290 Nigerian fintech companies surveyed in the 2020 Nigeria Fintech Census report are in the payment and remittance sub-sector.

Different views

Do the new entrants pose a threat to the older players? I don’t think so yet.

Early players, from before 2010, like Interswitch and eTranzact are focused on serving big companies and the government, while the new entrants are focused on SMEs and individuals. It’s understandable considering sunk costs and no foreign capital backing. Fintech analyst Maro Elias explains it:

“Fintech 1.0 players were content with serving largely bigger players which made sense considering payments is largely a scale business with 1.5% being the standard MSC (Merchant Service Charge) price for collections in Nigeria. The math makes sense if you look at it – it’s way more economically sound to serve a customer processing ₦200,000 ($482.71) in average transaction amount who pushes 10,000 transactions monthly capped at ₦2,000 ($4.83) than to serve a customer who pushes ₦5,000 ($12.07) in average transaction amount at 100,000 transactions monthly. Option one gives you ₦20 million ($48,270.7) a month in gross revenues, while option 2 gives you ₦3.75 million ($18101.5) a month in gross revenues, a clear 150%+ difference.”

Despite all the talk of fintech coming to displace banks, the banks responded a bit slower because the new entrants weren’t hurting their numbers and at best their customers’ needs were met by the new fintech companies.

In response to the rise of fintech companies, many major banks created fintech startup incubation programmes and started investing in existing fintech companies, acquiring or launching their fintech startup arm. An example of this is the EcoBank Challenge which identifies and partners with fintechs that are mature enough to scale. Guarantee Trust Bank, one of Nigeria’s largest banks, created Habari, to rival against the likes of Flutterwave and Paystack. In terms of partnerships, Neobanks like Kuda and Sparkle partner with existing traditional banks to handle some of their core banking functions.

There was some discomfort around how the fintech space wasn’t regulated enough, this often led to the sudden introduction of regulations. But over the years, numerous partnerships between fintech companies and financial institutions have reduced those clamours.

For the regulator despite being cautious and struggling to catch up, the rise of fintech startups has been a big win as an increase in financial inclusion is tied to the growth of the economy — Nigeria’s financial inclusion rate grew from 30% in 2010 to 45% by 2020. The fintech players also reduced the reliance on cash, fostering the government cash economy drive. A cashless economy has two implications: less money is spent on printing cash and the government has better visibility of how money is moving in the economy.

Consumers on the other hand are somewhat spoilt for choice on what services to use. Often sceptical about the reliability of new products but willing to try them out.

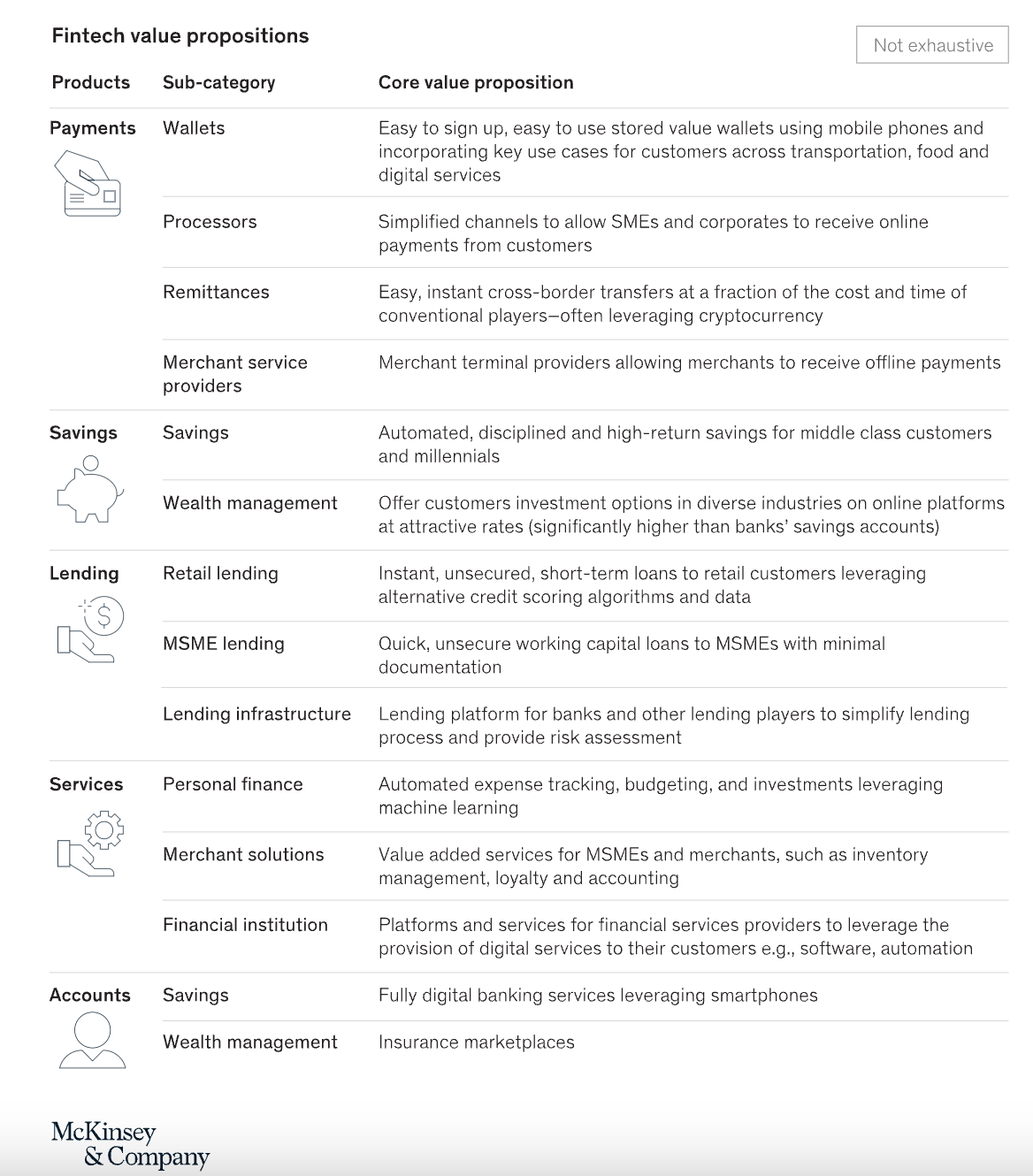

Image from a McKinsey report that identified a few opportunities (White space) in the African Fintech space.

What’s next?

The first generation of fintech companies laid the foundation for infrastructure, and with little foreign investor exposure, they chased profitability. The second generation is building on it by fostering the democratisation of financial services and chasing scale which will in turn lead to profitability.

To stand out fintech companies will have to do more, less or something entirely different.

Adding more features to a product or launching new products is an obvious differentiation tactic. Wealthtech platforms such as Piggyvest and Cowrywise have done this by evolving from just being savings platforms to including the ability for users to invest their funds into different investment options.

Flutterwave started in 2016 as a payment gateway for Africans and has today built an ecosystem of products such as lifestyle payments solution Barter, the Flutterwave Store and the Flutterwave Capital, which offers small businesses quick loans. MoniePoint has also done something similar, it went from building Point of Sale (POS) terminal applications for some of Nigeria’s biggest payment terminal service providers to building one of Nigeria’s largest business payment and banking platforms, with more than 400,000 businesses. It processes about $100 billion annually.

Increasing your product offerings gives you more opportunities to provide value to your existing and new customers, thereby creating more reasons for them to use your product. It’s important to note here that diversification can lead to spreading your resources too thin, thereby affecting the quality of the service you render.

Fintech companies can also opt to do less. In a world where many neobanks typically target the general population, female-focused fintech startup Herconomy went niche and decided to build a neobank for women. Instead of focusing on a broad market, consider a segment. It could be a savings platform for kids that doubles as a financial literacy platform.

Earlier, I pointed out that almost 50% of Nigerian fintech companies focus on payment and remittance. Another way fintech companies can stand out is by focusing on solving different and challenging problems.

Grey Finance was founded to solve the difficulties Nigerians faced when exchanging foreign currencies in their domiciliary accounts for Naira due to the country’s multiple exchange rates and scarcity of foreign exchange. Payourse is solving a similar problem by allowing people to change crypto to Naira. In addition, Payourse also built Simpa, a no-code tool that helps people build crypto exchanges within minutes.

For many operators in digital financial services, executing their business activities involves a lot of API integrations from many sources which could be time and money-consuming. Fortunately, a new wave of API fintech startups like One Pipe and Mono have chosen to do the legwork by aggregating different APIs and simplifying pricing such that integrations can go from 6 months down to 2 weeks.

On-demand salary access is a huge opportunity in Africa because millions of employees are trapped in an eternal debt cycle as they struggle to match their income to their daily expenses, emergencies, and opportunities. Startups like Earnipay are solving this problem alongside other Payroll tech companies.

Image from a McKinsey report that identified a few opportunities in the African Fintech space.

There’s still a lot of innovation that can happen in the web3 space beyond building crypto exchanges. Personal finance is due for more disruption as it can get more personalised. Regulation technology solutions, which deal with managing regulatory processes within the financial industry, can also be a game changer as many fintech companies strive to remain compliant.

Democratisation is the watchword for the future of technology and fintech won’t be any different. In the next 30 years, just maybe as Angela Strange famously postulated, “Every company will be a fintech company.”

Thanks to Victor for editing.